Financial Mistakes to Avoid in Your 20s and 30s

Financial Mistakes to Avoid in Your 20s and 30s — The financial choices you make in your early adulthood can shape your future wealth, security, and peace of mind. While your 20s and 30s are often filled with career growth and new responsibilities, they’re also a time when many people unknowingly make money mistakes that lead to long-term setbacks. From skipping retirement savings to mismanaging debt, this guide reveals the most common financial pitfalls young adults should avoid—and how to build smart money habits early for a more stable future.

1. Ignoring Budgeting and Expense Tracking

One of the biggest financial errors is not creating a monthly budget. Without knowing where your money goes, it’s nearly impossible to control spending or save consistently.

Budgeting doesn’t have to be complex. Use apps like YNAB, Mint, or even a simple spreadsheet. Categorize your spending, set limits, and track your habits regularly.

2. Living Beyond Your Means

In your 20s and 30s, it’s tempting to upgrade your lifestyle with every raise or job change. Social media also pressures many to match the lifestyles of friends or influencers, even if it leads to debt.

Living beyond your means often results in high-interest credit card balances and little to no savings. Focus on spending less than you earn. Practice delayed gratification and keep lifestyle inflation in check.

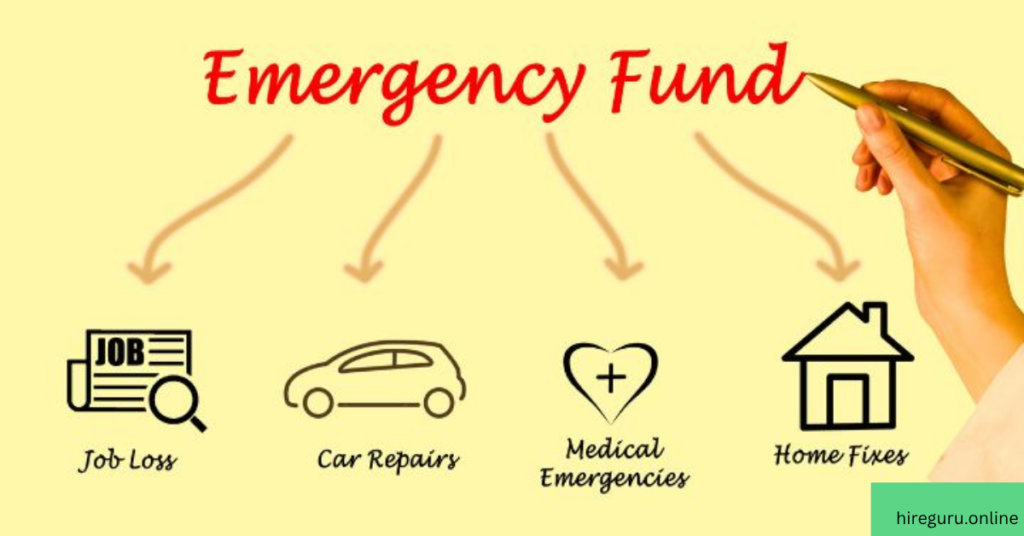

3. Failing to Build an Emergency Fund

Emergencies are inevitable. Whether it’s a medical bill, car repair, or sudden job loss, unexpected expenses can derail your finances if you’re unprepared.

Aim to save at least three to six months’ worth of living expenses in a high-yield savings account. Even starting with $500 and adding monthly can make a difference.

Relying on credit cards during emergencies leads to debt cycles that are hard to break.

4. Delaying Investing for Retirement

Many young adults postpone retirement savings, thinking they have plenty of time. But the sooner you start investing, the more you benefit from compound interest.

For example, saving $200/month starting at age 25 could grow to over $300,000 by age 60, assuming a 7% annual return. Waiting just 10 years could cut that amount in half.

Open a 401(k) if your employer offers one, and don’t miss out on employer match contributions. If not, consider a Roth IRA or Traditional IRA.

5. Not Managing Debt Strategically

Student loans, car loans, and credit cards are common in your 20s and 30s. The mistake isn’t having debt—it’s ignoring it or managing it poorly.

Prioritize high-interest debt first using the avalanche method, or start small for momentum with the snowball method. Always make at least the minimum payments on all debts to avoid penalties.

Consolidate or refinance loans when possible to lower interest rates.

6. Skipping Insurance Coverage

Insurance may seem unnecessary when you’re young and healthy, but accidents and illnesses can happen anytime.

Must-have insurance for young adults:

- Health insurance: Avoid medical debt

- Renter’s or homeowner’s insurance: Protect your property

- Auto insurance: Legal requirement and financial safety

- Term life insurance (if you have dependents)

Having the right coverage prevents catastrophic losses and helps you stay financially protected.

7. Not Building or Checking Your Credit Score

Your credit score affects more than just loans. It can impact apartment rentals, job applications, and even utility deposits.

Check your score regularly using free services like Credit Karma or your bank’s credit dashboard. Pay bills on time, keep credit utilization below 30%, and avoid opening too many new accounts at once.

Start building credit early to qualify for lower interest rates later in life.

Also Visit This Cryptocurrency vs Stock Market

8. Ignoring Financial Education

Not learning about money is a mistake that keeps you dependent on others—or worse, leads to financial ruin.

Self-education is now easier than ever. Read books like “The Psychology of Money” or “Rich Dad Poor Dad”, listen to podcasts, or take free online financial literacy courses.

Knowledge about investing, budgeting, and credit empowers you to make better decisions and avoid scams or bad habits.

9. Not Setting Financial Goals

Many young people drift through their financial life without specific goals. This leads to missed opportunities and poor habits.

Set short-term and long-term goals:

- Short-term: build an emergency fund, pay off credit card debt

- Mid-term: save for a car, plan a vacation

- Long-term: invest for retirement, buy a home

Write your goals down, review them monthly, and adjust as needed. Goal-setting gives your money purpose and direction.

10. Not Taking Advantage of Employer Benefits

If your job offers benefits like retirement plans, health savings accounts, or tuition reimbursement, don’t ignore them.

Many people miss out on free money in the form of 401(k) matches or flexible spending accounts (FSAs) because they don’t read their benefits package.

Talk to HR, ask questions, and fully understand your employment benefits—they can save or earn you thousands over time.

Conclusion: Learn Early, Prosper Later

Making financial mistakes in your 20s and 30s isn’t the end of the world—but avoiding them gives you a huge advantage. Small, consistent financial habits today can lead to a future filled with freedom, opportunity, and less stress.